Policy Changes and Economic Repositioning: The Prescription for People and Pharma to Pull Through Uncertainties

Review of First Quarter 2025

The first quarter of 2025 was marked by widespread turmoil, chaos, and uncertainty, which gripped both investors and the general public, threatening to escalate a seemingly contained financial crisis into a self-inflicted global economic catastrophe with far-reaching consequences.

The previously published Healthcare Executive Highlights for the fourth quarter of 2024 noted the evolving environment in which the U.S. Federal Reserve Bank (Fed) operates. It was unexpected how quickly these concerns would materialize when President Trump began urging the Fed to cut rates(1,2) in an effort to prevent the escalation of an impending crisis that fortunately was avoided.

The Trump administration has cut ties with the past by introducing a set of unprecedented policy changes that aim to maximize efficiency across the board. Healthcare has experienced this from day one with decisions such as the following:

Withdrawal from the World Health Organization (WHO). This decision is likely to have minimal impact on the United States healthcare system. Although some might argue about epidemics and pandemics, these risks are largely mitigated by the robust preventive measures supported by the United Nations International Children’s Emergency Fund (UNICEF).

National Institutes of Health funding. Universities and academic hospitals are beginning to experience the effects of the National Institutes of Health’s (NIH) new research funding policy, which has disrupted their ongoing studies and trials. Despite efforts by some advocates to promote pro-research funding policies, their voices have not been strong enough to highlight the remarkable successes achieved through science funding. As a result, research budget cuts appear inevitable in the absence of stronger advocacy.

In the realm of healthcare, the essence of the new policy appears to emerge from the contrast between the 2025 Economic Report of the President to Congress and the response from the Joint Economic Committee.(3,4) Whereas the previous president and the Democrats emphasized health insurance coverage, the current president and the Republicans prioritize fiscal responsibility, efficiency, and innovation, especially concerning diseases such as obesity that pose significant public health and financial challenges.

The outcome of this significant policy overhaul is an unprecedented level of uncertainty, which, unsurprisingly, has had serious repercussions for both individuals and policymakers, as follows:

Consumer sentiment, according to the Michigan University Index, has tanked sharply during the first quarter, shedding 23% of its end-of-2024 level (from 74.0 during December down to 57.9 in March).(5) Similarly, the proportion of those anticipating an uptake in unemployment has reached its highest level since 2009.(6)

Uncertainty has fueled the Fed leaders’ concerns about the outlook of the economy, as manifested by their assessment of heightening uncertainty and risks to major economic indicators such as gross domestic product (GDP), unemployment, and personal consumer expenditure (PCE).(7)

Gross Domestic Product

The GDP of the last quarter of 2024 showed an increase of 2.4% on the third estimate. On top of sectors that contributed to the expansion of the U.S. economy came healthcare, which witnessed the largest sectoral increase, by 32.8% and 48.5%, in the fourth and third quarters of 2024, respectively.(8)

The quarterly projections for the second quarter indicate strong headwinds, mainly attributed to federal spending cuts and the trade war.

For the 2025 and 2026 annual predictions of the U.S. GDP, the American economy might show some signs and pockets of weakness secondary to federal rebudgeting and the trade war; however, the overall picture might not be as dark as predicted by leading organizations (Figure 1).

Figure 1. U.S. GDP estimates for 2025 and 2026.(9-12)

Fiscal and Monetary

Fiscal policy recently has undergone a significant transformation, perhaps the most dramatic in recent history. President Trump is expected to address both facets of fiscal policy: government spending and taxation. To tackle the former, he created the Department of Government Efficiency (DOGE), which immediately began aggressively reducing government expenditures. On the taxation front, President Trump campaigned on the promise of tax reforms, and the path to implementation appears straightforward, provided there is alignment between the executive and legislative branches of the U.S. government.

Monetary policy also has evolved, with the Fed operating in a significantly more challenging environment marked by uncertainty and confrontations, as predicted. Despite these obstacles, the Fed has shown no signs of yielding, firmly maintaining its stance. This resolve has been demonstrated through both its words and actions, as follows:

Words. Fed President Jerome Powell has reaffirmed a central message in two of the speeches he gave during April, which is that the Fed is a nonpolitical entity.(13,14)

Actions. The Fed has held interest rates unchanged at 4.25% to 4.50% twice during its January and March meetings.(15,16)

Inflation and Prices

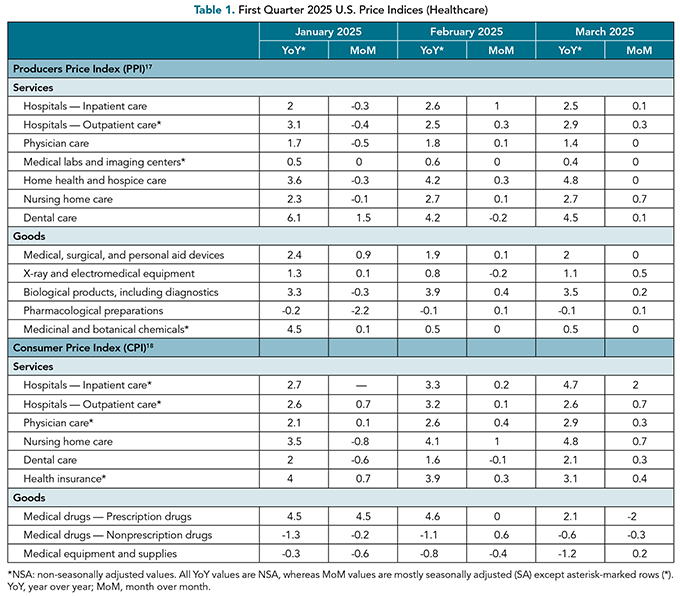

Regarding the Consumer Price Index (CPI), the monthly figures presented a somewhat mixed picture (Table 1). However, annual inflation has shown signs of cooling compared with the last quarter of 2024, moving closer to the elusive 2% target. Shelter-fueled inflation hikes reported during the first two months account for about 30% and 50% of the reported increase during those two months, respectively. The overall CPI for March was significantly influenced by favorable energy prices during that period. Meanwhile, the healthcare CPI remained relatively stable, fluctuating between 0.2% and 0.3% monthly over the same timeframe.

Monthly and yearly inflation numbers reported during the opening quarter of 2025 are summarized as follows:

January CPI = 3.0% (YoY); 0.5% (MoM);

February CPI = 2.8% (YoY); 0.2% (MoM); and

March CPI = 2.4% (YoY); -0.1% (MoM).

A similar start for 2025 was noticed in the producer price index (PPI) with a much broader range of monthly figures (between 0.6% and –0.4%). However, annual numbers showed a steady decline throughout the first 3 months of 2025, reversing the course of the preceding quarter. Details of these numbers are as follows:

January PPI = 3.5% (YoY); 0.4% (MoM);

February PPI = 3.2% (YoY); 0.6% (MoM); and

March PPI = 2.7% (YoY); -0.4% (MoM).

Personal consumer expenditure (PCE) remains consistent with the last three reports of 2024; however, the numbers tell so much more about the underlying dynamics and trends:

Cheaper energy masks the consumer appetite to spend. During January, the numbers came pretty much in line with estimates for both headline and core PCE. In February, the 2.8% core PCE came in a little hotter than expected, but this was offset by declining energy prices, which mitigated impact on the headline PCE annual number.(19,20)

January headline vs core PCE = 2.5% vs 2.6% (YoY); 0.3% vs 0.3% (MoM).

February headline vs core PCE = 2.5% vs 2.8% (YoY); 0.3% vs 0.4% (MoM).

Consumers are driven by practical decisions, not emotions. January real-dollar PCE showed a $30.7 billion drop in spending, which is the net of $76.7 billion cuts in spending on goods and the $46 billion increase in services spending. In contrast, February witnessed a remarkable uptake in real-dollar PCE by $87.8 billion, the result of the $56.3 billion and $31.5 billion spent on goods and services, respectively.(19,20)

Although this is likely to be a temporary trend as consumer exhaustion sets in, it is one of the most striking examples of such behavior. Initially, consumers held on to their cash in January, anticipating the expected tariffs. However, in February, it appears that they made the economically sound decision to stock up as much as possible before the tariffs took effect.

Labor and Productivity

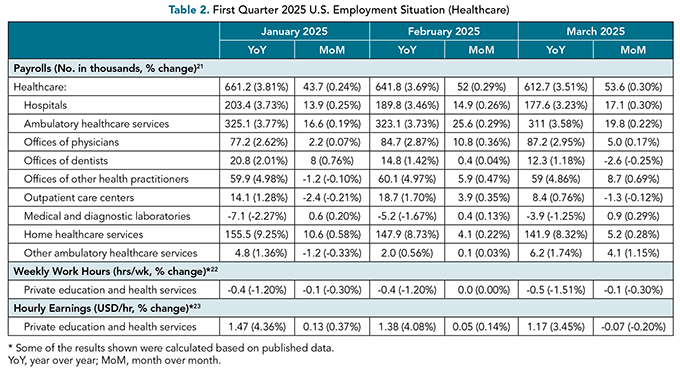

The new federal policy and the resulting uncertainty have negatively impacted the U.S. job market, leading to a clumsy start for 2025 (Table 2). January employment numbers failed expectations, with new payrolls numbering 143,000 versus estimates of 170,000, and the unemployment rate shed 0.1%, hitting its lowest level since May of 2024 (4%).(24) Likewise, February new jobs came in slightly lower than expected (151,000 versus 160,000) with the unemployment rate ticking up once again to 4.1%.(25) March has seen a strong comeback for non–farm payrolls with 228,000 jobs added, far more than the estimated 140,000. Unemployment numbers continued to climb up, to reach 4.2% in March.(26)

Looking Toward Second Quarter 2025

The 90-day grace period granted by President Trump to most countries before the reinstatement of reciprocal tariffs will significantly influence the landscape during the second quarter and beyond. Although some view this interval as a temporary reprieve before the inevitable resurgence of tariffs, it is believed that numerous trade agreements and deals are likely to be finalized within this timeframe. It is important to note that progress will vary greatly and be specific to each country. For example, reaching an agreement with countries such as China will be particularly challenging, whereas negotiations with the United Kingdom are expected to be much more straightforward.

Similarly, it is believed that sector-specific tariffs could impact the healthcare and pharmaceutical industries as early as the second quarter, given the recently announced federal investigation under Section 232. This investigation encompasses various elements, including active pharmaceutical ingredients, finished dosage forms, and medical countermeasures, among others.(27) Notably, approximately 85% of branded medications in the United States are composed of imported components, with 43% of active pharmaceutical ingredients sourced from European countries.(28)

Another trend to monitor is the employment situation in light of federal government layoffs and the new policy directions. It is predicted that this will start to fully materialize in employment numbers over the course of the second and third quarters.

References

Ackerman A. Trump is pressuring the Fed to cut rates. Here’s why it probably won’t. The Washington Post. April 8, 2025. www.washingtonpost.com/business/2025/04/08/trump-fed-powell-interest-rates/ .

Jackson K, Shakil I. Trump says ‘perfect time’ for Fed to cut interest rates. Reuters. April 3, 2025. www.reuters.com/world/us/trump-says-perfect-time-fed-cut-interest-rates-2025-04-04/ .

Executive Office of the President of the United States. Economic Report of the President and the Annual Report of the Council of Economic Advisers. January 2025. https://bidenwhitehouse.archives.gov/wp-content/uploads/2025/01/ERP-2025.pdf .

U.S. Joint Economic Committee. The 2025 Joint Economic Report: Report of the Joint Economic Committee, Congress of the United States on the 2025 Economic Report of the President (Report No. 119-9). March 3, 2025. www.jec.senate.gov/public/_cache/files/962ebb89-1460-4c7f-b014-9a6307f4bd5e/the-2025-joint-economic-report-119th-congress-.pdf .

Hsu J. Preliminary results from the March 2025 survey. University of Michigan’s Surveys of Consumers. March 14, 2025. https://data.sca.isr.umich.edu/fetchdoc.php?docid=78219 .

Hsu J. Preliminary results for April 2025. University of Michigan’s Surveys of Consumers. April 11, 2025. www.sca.isr.umich.edu/files/featured-chart.pdf .

Federal Open Market Committee (FOMC) and Board of Governors of the Federal Reserve System. March 19, 2025. FOMC Projections materials: accessible version. www.federalreserve.gov/monetarypolicy/fomcprojtabl20250319.htm .

U.S. Bureau of Economic Analysis. Table 3. Gross domestic product: level and change from preceding period. In: Gross Domestic Product (Third Estimate), Corporate Profits, and GDP by Industry, 4th Quarter and Year 2024. www.bea.gov/sites/default/files/2025-03/gdp4q24-3rd.pdf .

Saraiva A, Morgan D. Economists say trade war makes US recession almost a coin flip. Bloomberg. April 25, 2025. www.bloomberg.com/news/features/2025-04-25/economists-say-trade-war-makes-us-recession-almost-a-coin-flip .

Kalish I, Gibbard R. United States Economic Forecast. Deloitte Global Economics Research Center. March 26, 2025. www2.deloitte.com/us/en/insights/economy/us-economic-forecast/united-states-outlook-analysis.html.

Panday S, Das D, Bhattacharya A, Biswas A. Economic research: economic outlook U.S. Q2 2025: losing steam amid shifting policies. S&P Global. March 25, 2025. www.spglobal.com/ratings/en/research/articles/250325-economic-outlook-u-s-q2-2025-losing-steam-amid-shifting-policies-13450076 .

Goldman Sachs Research. Why the US economy may grow more slowly than expected. March 13, 2025. www.goldmansachs.com/insights/articles/why-the-us-economy-may-grow-more-slowly-than-expected .

Hon. Jerome H. Powell, Chair, Board of Governors of the Federal Reserve System, 4/16/25. The Economic Club of Chicago, April 4, 2025. Video: 57:10 min. www.youtube.com/watch?v=1o_9kO0zZQg .

LIVE: Fed Chair Jerome Powell speaks at a conference in Virginia. Associated Press. April 4, 2025. Video: 38:55 min. www.youtube.com/watch?v=HnFZLA0qdC8 .

U.S. Federal Reserve System. Press Release. 29 January 29, 2025. www.federalreserve.gov/monetarypolicy/files/monetary20250129a1.pdf .

U.S. Federal Reserve System. Press Release. March 19, 2025. www.federalreserve.gov/monetarypolicy/files/monetary20250319a1.pdf .

U.S. Bureau of Labor Statistics. Table 2. Producer price index percent changes for selected commodity groupings by Final Demand - Intermediate Demand category, seasonally adjusted. Last modified April 11, 2025. www.bls.gov/news.release/ppi.t02.htm .

U.S. Bureau of Labor Statistics. Table 2. Consumer price index for all urban consumers (CPI-U): U. S. city average, by detailed expenditure category. Last modified April 10, 2025. www.bls.gov/news.release/cpi.t02.htm .

U.S. Bureau of Economic Analysis. Personal income and outlays, January 2025. February 28, 2025. www.bea.gov/sites/default/files/2025-02/pi0125_0.pdf .

U.S. Bureau of Economic Analysis. Personal income and outlays, February 2025. March 28, 2025.www.bea.gov/sites/default/files/2025-03/pi0225.pdf .

U.S. Bureau of Labor Statistics. Table B-1. Employees on nonfarm payrolls by industry sector and selected industry detail. Last modified April 4, 2025. www.bls.gov/news.release/empsit.t17.htm .

U.S. Bureau of Labor Statistics.. Table B-2. Average weekly hours and overtime of all employees on private nonfarm payrolls by industry sector, seasonally adjusted. Last modified April 4, 2025.www.bls.gov/news.release/empsit.t18.htm .

U.S. Bureau of Labor Statistics. Table B-3. Average hourly and weekly earnings of all employees on private nonfarm payrolls by industry sector, seasonally adjusted. Last modified April 4, 2025. www.bls.gov/news.release/empsit.t19.htm .

Mutikani L. Moderate US job growth expected in noisy January employment report. Reuters. February 7, 2025. www.reuters.com/markets/us/moderate-us-job-growth-expected-noisy-january-employment-report-2025-02-07/ .

Dwyer C. US unemployment ticks slightly higher, economy adds 151K jobs in February. J.P.Morgan Wealth Management. March 10, 2025. www.jpmorgan.com/insights/outlook/economic-outlook/jobs-report-february-2025 .

Dwyer C. U.S. adds 228K jobs in March amidst market volatility: how investors should read the numbers. J.P.Morgan Wealth Management. April 7, 2025. www.jpmorgan.com/insights/outlook/economic-outlook/jobs-report-march-2025 .

Brown A. Pharma tariffs could leave little room to hide with sweeping probe underway. Endpoints News. April 15, 2025. https://endpts.com/trumps-pharma-probe-sweeps-in-apis-key-starting-materials/ .

Brown A. US drugs rely heavily on ingredients made overseas, new report shows. Endpoints News. April 17, 2025. https://endpts.com/us-drugs-rely-heavily-on-ingredients-made-overseas-report/ .